The last 18 months have seen the biggest ever change in the window, door and conservatory industry.

Jade Greenhow, Operations Director of award-winning specialist data supplier Insight Data, revealed the facts and figures that point to an industry evolving and consolidating, with clear winners emerging as new opportunities present themselves.

Fabricators and installers

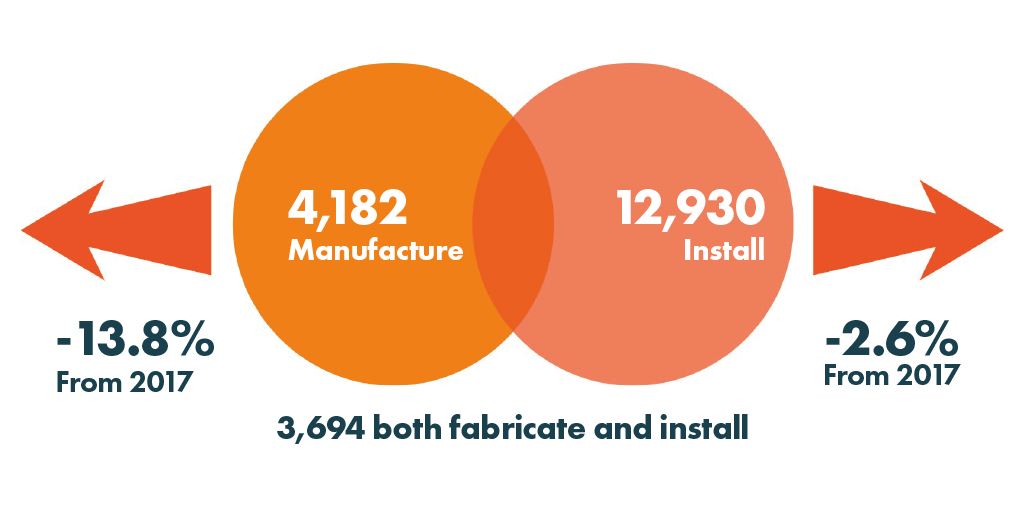

With 4,182 companies currently manufacturing products, this is a sharp decline from 4,800 in 2017. The picture is skewed, however, as more than 50% of manufacturers are timber joinery firms and it is this segment of the market that has seen the biggest decline.

Meanwhile, just under 13,000 companies are installers operating in the retail, new-build or commercial sectors, which has also declined marginally from 2017.

There is a significant overlap, as 3,700 sit in both categories by installing and manufacturing at least some products.

The definition used to be quite clear – with installers who manufactured and those who ‘bought in’ from a fabricator.

However, that line is blurring more and more, with installers offering a wider product range from multiple suppliers, often giving consumers a good, better and best solution.

PVC-U fabricators

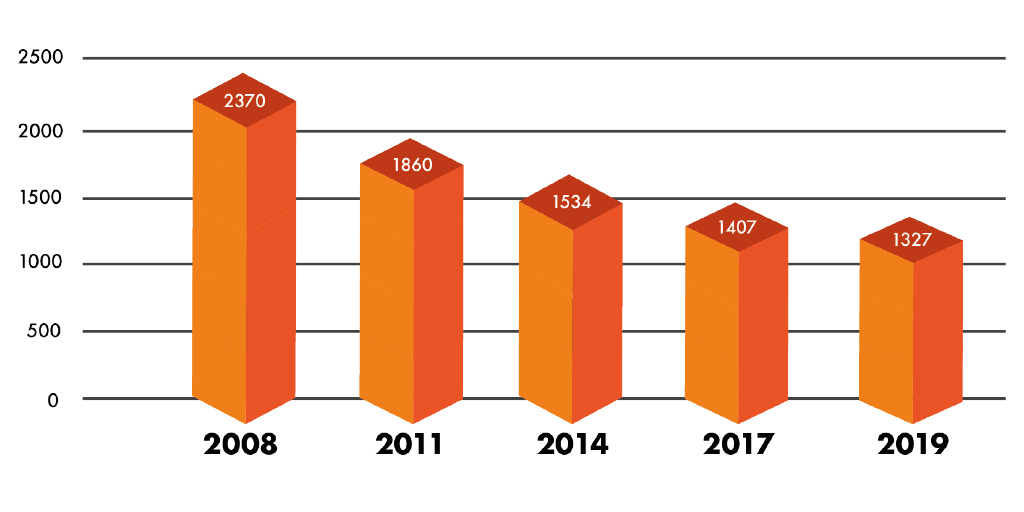

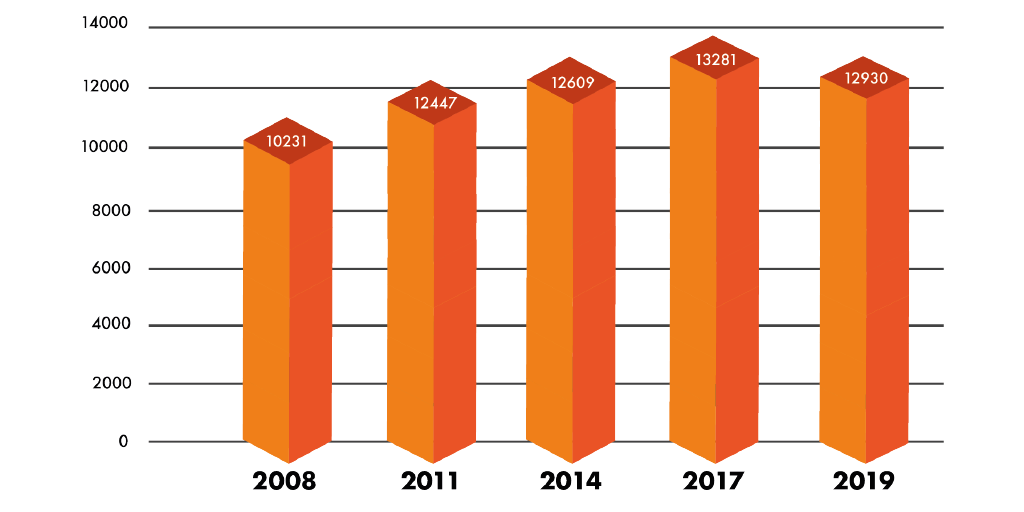

Taking a longer-term look at the market highlights perhaps the single biggest shift across the industry – a huge decline in PVC-U fabricators, with a staggering 1,000 companies ceasing manufacturing since 2008.

However, it’s not all doom and gloom, and most PVC-U fabricators are positive about their business and most have seen revenue growth.

Indeed, the market does appear to have stabilised in the last two years, with just 80 firms from the smaller end of the market withdrawing from fabrication.

This has meant that those remaining have benefitted from absorbing the additional volume released into the market.

Fabricators, particularly larger ones, are diversifying their product range to maintain revenue and margins and protect their customer base.

Many PVC-U fabricators now manufacture or offer aluminium as well as premium PVC-U products, including flush sash and coloured frames, and it’s clear these are the key drivers for the industry.

We are now seeing this cascade up the supply chain and it’s no surprise several PVC-U systems companies are moving into aluminium and we expect to see significant activity in this space as PVC-U systems companies re-think their own business model.

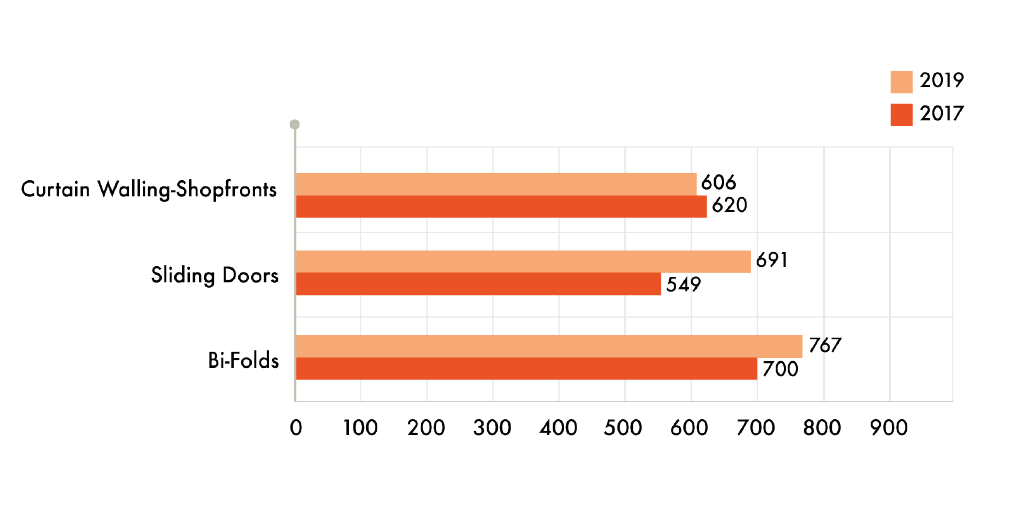

Aluminium fabricators

With a resurgence in residential aluminium products it’s no surprise that the number of fabricators has risen 9% to 870 companies since 2017.

And with the commercial market remaining volatile, particularly for fabricators working with main contractors and house-builders, some aluminium fabricators have moved from commercial into the more lucrative trade and retail markets.

There is now a shift from bi-fold doors to aluminium sliding doors, with installers reporting increasing interest in large-span sliders both for refurbishment and increasingly single-storey extensions.

There is, though, one untapped opportunity – aluminium entrance doors. Several companies have launched premium entrance solutions, but this market is still dominated by composite doors.

Installers

The number of installers has declined slightly over the last two years but, at almost 13,000 firms, this is still significantly higher than 10 years ago.

We’ve seen a rapid increase in M&A activity in recent times. For some, it is a fast-track way to scale up, enter new markets or secure customers.

For those without the appetite for major growth or investment, perhaps approaching retirement, it is an ideal opportunity to exit.

Installers have also diversified. A much wider range of products, materials and options have emerged in recent years and this has enabled them to expand their offering. This does mean, however, that they are now sourcing from multiple suppliers.

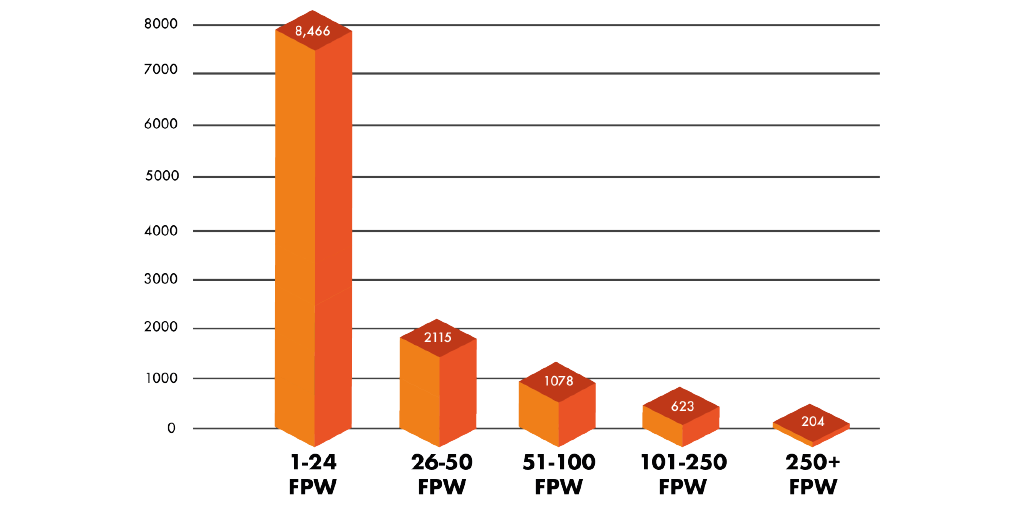

Installers by volume

The industry is still dominated by small installers, typically lifestyle businesses operating from home or a lock-up, with 68% installing between 1-25 frames per week.

They are increasingly sourcing products from trade counters who provide the storage and product range that installers want.

But they do face several risks, including having the resources to meet some customer needs. This has seen local builders winning market share, particularly in the glazed extension and sliding door markets, where they are sourcing products from trade counters and builders’ merchants.

At the other end of the scale are larger regional and national installers. While some of these have fared better than others, most have had a tough time with poor financial performance.

The ‘sweet spot’ appears to be the middle ground, owner-managed businesses between 50 – 250 frames per week, many of which are healthy, growing businesses.